The Government of Nepal, through the newly introduced Finance Act, 2083, has launched a highly encouraging tax amnesty and relief scheme under Section 32 to Section 49. This special provision aims to bring unregistered taxpayers into the formal tax net, allow inactive taxpayers a clean exit or restart opportunity, and provide substantial interest and penalty relief to existing compliant taxpayers who have fallen behind on their filings.

Taxpayers have a strict deadline until Poush-end, 2083 to leverage these waivers. Below is an in-depth breakdown of the three major categories of benefits introduced under this special provision.

Understanding the Special Income Tax Interest & Fee Waiver Scheme (Finance Act, 2083)

1. Opportunity for Unregistered Individuals (New Taxpayer Relief)

For individuals or entities that have earned taxable income in the past but never registered for a Permanent Account Number (PAN) or filed tax returns, the government offers a complete waiver of historical liabilities under the following terms:

- Requirement: The individual must obtain a PAN and submit their income tax returns specifically for the Fiscal Years 2079/080 through 2082/083.

- Financial Relief: Upon payment of the principal tax assessed for these specified years, all applicable fees, penalties, and interest will be completely waived.

- Historical Immunity: Most importantly, they will not be required to submit tax returns, nor pay any taxes, fees, or interest for any fiscal years prior to FY 2079/080.

2. Relief for Inactive or Non-Filing PAN Holders

This provision targets registered taxpayers who possess a PAN but have not conducted business activities or filed returns for FY 2081/082 or earlier. They are given two choices before the deadline:

- Option A (Business Resumption / Activation): If the taxpayer wants to actively resume operations, they must file the tax return and pay the regular tax for FY 2082/083 by Poush-end 2083. Upon doing so, all outstanding returns and tax obligations for the years prior to FY 2082/083 are fully waived.

- Option B (Official De-registration / Exit): If the taxpayer wishes to permanently close their tax registration, they can apply for de-registration by filing the return for FY 2082/083, without having to clear previous years’ backlogs.

⚠️ CRITICAL WARNING: If an inactive taxpayer fails to file an application for either activation or de-registration within the Poush-end 2083 deadline, their PAN will be automatically canceled by the Integrated Tax System. If they wish to reactivate it in the future, they will be forced to submit all historical missing returns and pay full taxes, accumulated fees, and penal interest for the entire block period.

3. Relief for Existing PAN Holders with Outstanding Dues

For taxpayers registered under the Income Tax Act, 2058 who have generated taxable income but have outstanding tax liabilities and unsubmitted returns, the government offers a structured penalty settlement plan:

- The Package: Taxpayers must pay the principal outstanding tax amount along with an additional 1% of the tax amount as a nominal settlement charge.

- The Benefit: If this payment and the corresponding returns are submitted by Poush-end 2083, the system will completely waive all applicable interest and late fees.

How to get PAN Tax Vat Excise Kar Chhut Waiver Scheme Online

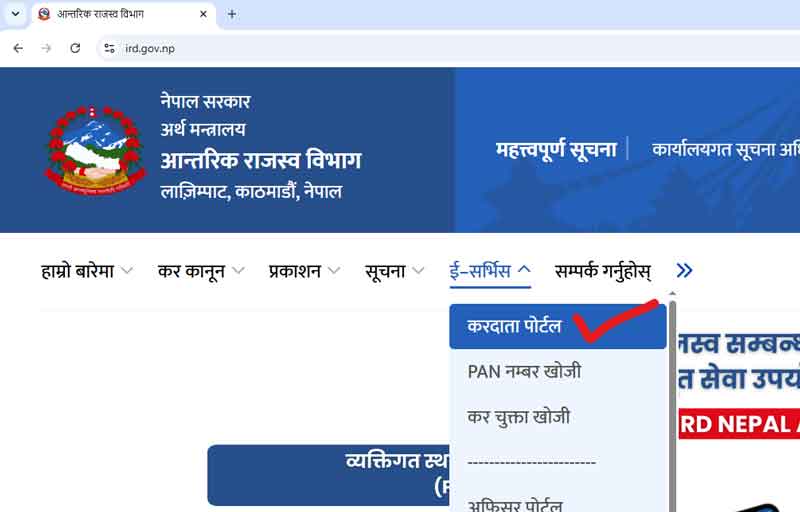

Step 1: Access the Taxpayer Portal

- Navigate to the official IRD website at

ird.gov.np. - Hover over or click on the (E-Services) menu on the main navigation bar.

- From the dropdown menu, select (Taxpayer Portal) as highlighted with the checkmark in “tax scheme 1.png”.

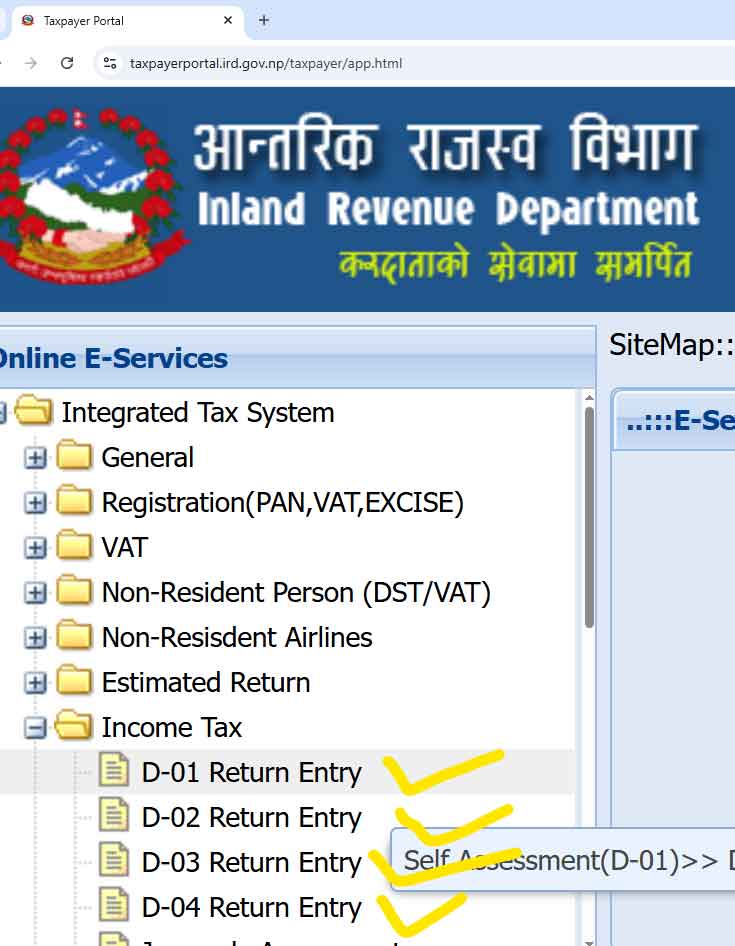

Step 2: Navigate to Income Tax Return Entry

- Once inside the Taxpayer Portal, look at the left sidebar menu under the “Online E-Services” section.

- Expand the “Income Tax” folder.

- Click on “D-01 Return Entry” and select the sub-option “Self Assessment(D-01)” as shown in “tax scheme 2.png”.

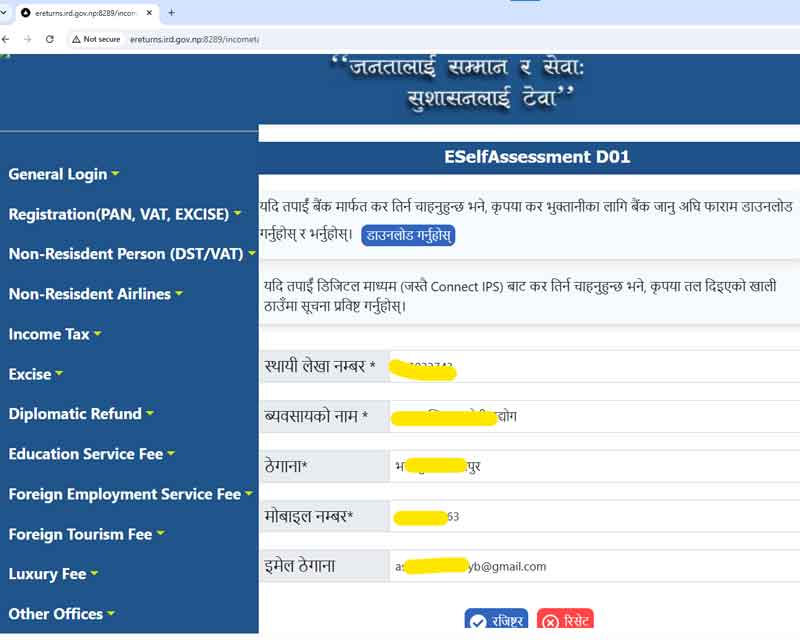

Step 3: Register for E-Self Assessment

- You will be redirected to the

ereturns.ird.gov.npportal for the ESelfAssessment D01 form. - Fill in your basic details required for registration, including:

- Permanent Account Number – PAN)

- Business Name)

- Address)

- Mobile Number)

- Email Address)

- Click the blue (Register) button at the bottom as illustrated below.

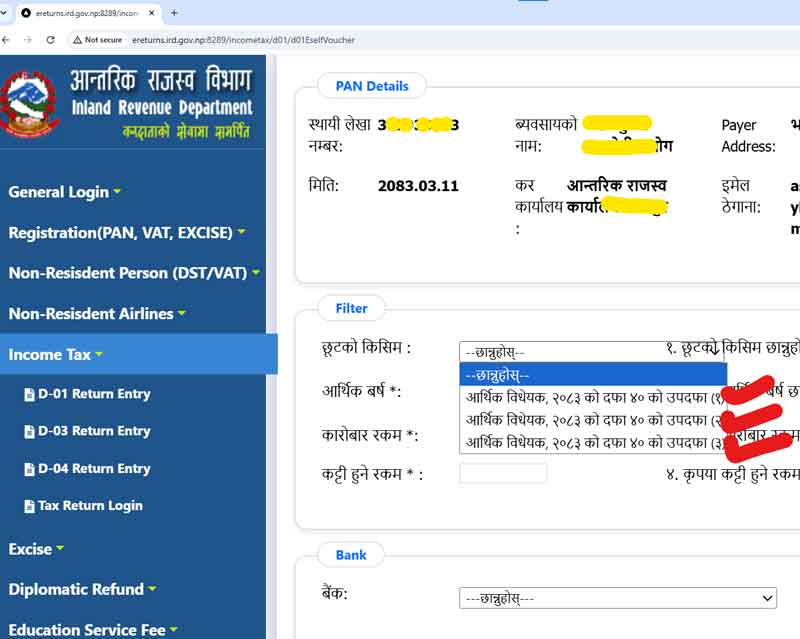

Step 4: Choose the Tax Discount Scheme Provision

- Once logged in, go to the Filter section of the voucher generation system.

- Click on the dropdown menu for (Type of Discount / Waiver).

- As shown in , select the specific amnesty clause from the list matching your eligibility under Section 40 of the Finance Act, 2083:

- Option 1: Subsection (1) for completely unregistered individuals.

- Option 2: Subsection (2) for inactive/non-filing PAN holders looking to activate or exit.

- Option 3: Subsection (3) for existing PAN holders seeking the interest and fee waiver by paying the 1% additional fee.

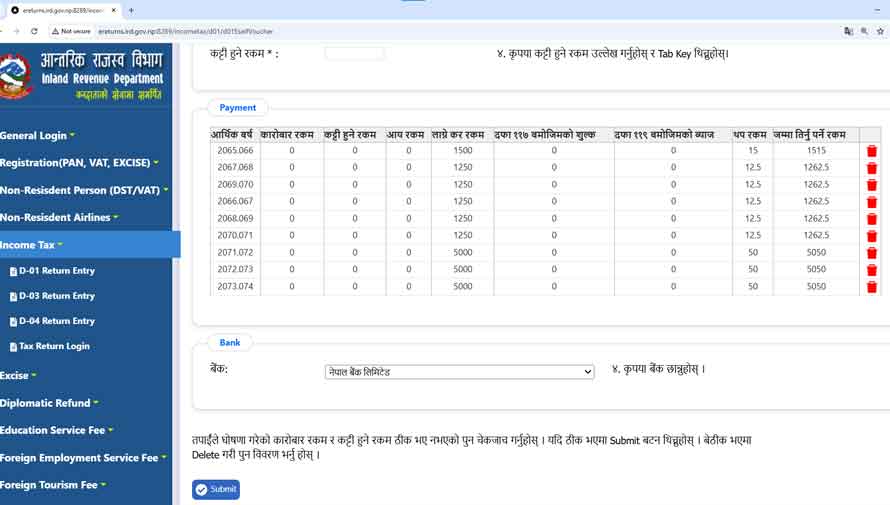

Step 5: Verify Calculations and Bank Details

- After selecting the scheme and inputting your relevant (Fiscal Year), the portal will automatically load your tax table.

- As visible in, notice that the columns for Section 117 Fees and Section 119 Interest are completely calculated as 0 under the waiver. Only the base tax and the nominal additional amount make up your total payable amount.

- Choose your preferred (Bank) from the dropdown menu (e.g., Nepal Bank Limited).

- Thoroughly double-check the amounts and hit the blue “Submit” button at the bottom.

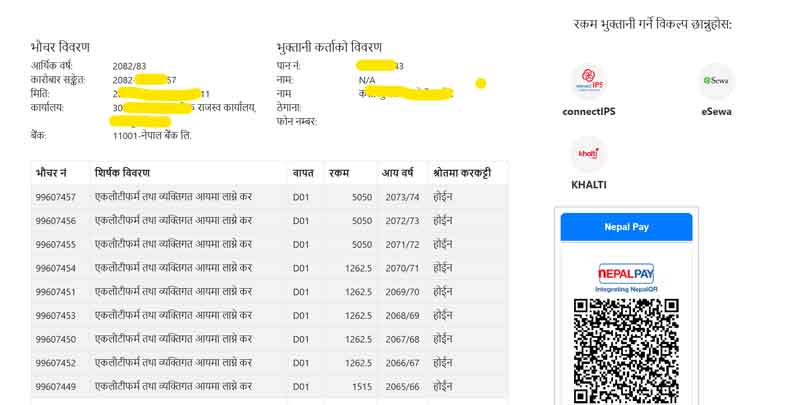

Step 6: Make the Online Payment

- The system will generate your online tax payment voucher details containing your Transaction ID and a breakdown of the specific fiscal years being paid.

- On the right side of the screen, as shown in QR, choose your preferred digital wallet or payment gateway:

- connectIPS

- eSewa

- KHALTI

- Nepal Pay / QR Scan

- Complete the digital transaction to instantly finalize your tax compliance under the amnesty scheme.

=> Apply Online Tax Discount Scheme Waiver from the IRD

Key Takeaway for Taxpayers

This scheme represents one of the most generous tax amnesties provided recently by the Inland Revenue Department (IRD). Whether you are looking to formalize an unregistered business, close down an old dormant entity without paying heavy fines, or settle accumulated tax debts, you must act before the deadline of Poush-end, 2083. Failing to do so will result in strict automated system penalties and loss of amnesty privileges.